When you’re a kid, the big dilemma you face is whether to spend your allowance on candy or ice cream. When you’re a teen it becomes: do I go to university or take a year off and travel? Then when you hit adulthood it shifts to: do I continue to rent or buy? The renting vs buying a house debate is what a lot of millennials are facing right now and if you happen to overhear them talking about it, you may hear them refer to the latter as “adulting.” Choosing to buy a home is a very adult move, especially in this day and age. And while I’m sure it was for our parents’ generation too, it just seems that it is a dream that has become that much harder for young adults today to actually attain — especially for those of us living in Toronto.

With Toronto having the highest rental prices in the country, this dilemma of renting versus buying is even more prevalent. It’s harder to ignore the fact that by renting you’re literally throwing away tens of thousands of dollars a year. So is it better to keep paying the outrageously high price to rent in Toronto or should you use those same funds towards your very own home or condo instead? The truth is, there’s no right or wrong answer — it really depends on the individual. The two biggest factors to consider are whether or not you are financially and emotionally ready to buy.

One of the benefits to renting vs owning is the flexibility. By renting, you’re not locked in to one place for years to come. Maybe a job opportunity comes up in another province or another country. If you’re renting, that’s an easy fix.

If you picture yourself living in Toronto for the next five to ten years, I’d say that buying a property may be worth considering. Let’s be honest, even if you need to relocate for whatever reason you’re still able to rent out your property, earning you some extra income that can help pay down your mortgage.

But location isn’t everything. Being a homeowner has its challenges. Are you ready to take on the extra responsibilities of being a homeowner? Living the life of a renter has its perks. Overall, it is very hassle-free. Say, your fridge stops working. Guess what? While you may need to feast on everything that’s in there, you don’t have to spend a dime to replace it. You don’t have to worry about any maintenance or repairs. If something needs to be repaired — or worse yet — needs to be replaced, it has no impact on your budget or your mentality. It’s a very stress-free way of life.

However, if there are things you want to alter, update, or renovate — you’re sh*t out of luck. What you see is what you get. Even if your landlord did allow you to make any changes, at the end of the day it’s to the advantage of their property, not yours. It’s a bit of a trade-off: as a homeowner you’re faced with a whole new series of responsibilities, but — you also have full control of your property.

Related: Move Or Renovate: Pick What’s Best For You!

Financials are the biggest hurdle of all. The biggest factor for those who are still renting is that they simply can’t afford to buy. To buy a property in Toronto you need to be able to put at least 5% down, though 20% is ideal. If you put less than 20% down, you will need to pay mortgage insurance which, beyond a higher mortgage overall, will contribute to higher monthly carrying costs. But if you can afford the higher monthly costs that come with 5% down, you’re still able to start building equity for yourself right away. Use our Mortgage Calculator to see what your monthly costs could be.

With 20% down on a $500K condo, you’re looking at $100K in hard cash. (If that was a rude awakening, I’d start saving now.) There are ways to help get you that down payment.

Let’s hope Mom and Dad are feeling generous. Did you know they can actually gift you a down payment of as much or as little as they want and there are no tax implications? Similarly, you can use up to $25K of your RRSP savings (or twice that if you’re a couple) towards that down payment. For more on how to save, read our Step-by-Step Guide to Saving for a Down Payment

Alternatively to buying resale, buying a pre-construction condo is a great way to buy your first home. When you buy a pre-construction condo, you are able to purchase properties with a payment structure that is easier on your wallet. Rather than 20% up front, you’ll typically pay 15% over the first year with no more payments kicking in, not even your mortgage, until the building takes occupancy 3 to 4 years later. All the while, you’re earning equity as the property is being built. Our pre-construction strategy helps ensure you have access to properties that are carefully picked with great profit potential. Check out some of our client returns here.

Learn all about Investing in Pre-construction Toronto Condos with this free guide

To help cover some of the expenses involved with buying a home, there are some rebates in place to help first-time homebuyers. The first is a $750 First-time Home Buyers’ Tax Credit and the second is a Land Transfer Tax Rebate for First-time Home Buyers which, if eligible, can earn you a full or partial refund on your Land Transfer Tax.

We make it easy to answer the question, “Is it better to rent or buy in Toronto?” by breaking down the math for you below on the cost of renting vs owning your own condo.

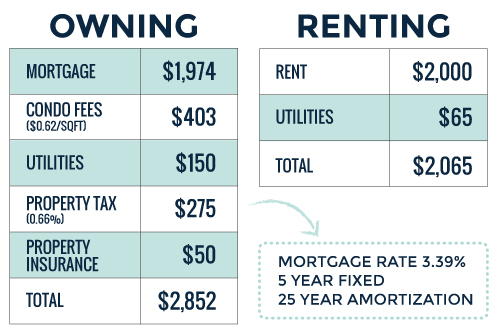

Let’s say you can swing the down payment on that $500K property. How will your monthly expenses compare when buying vs renting? In addition to your monthly mortgage payment, you will need to pay condo fees, property taxes, property insurance, and utilities. Let’s compare expenses of owning versus renting a 650sqft one-bedroom condo in downtown Toronto.

Comparatively, a condo that costs you $2,065/month to rent will cost you $2,852/month to own. That’s just shy of an $800 difference. There’s no denying that the carrying costs affiliated with owning your own property are much higher but that extra $800 is roughly the portion of your monthly expenses that’s paying your mortgage principal (see chart below). Think of it as a forced savings account. Or better yet, think of how much money you’ve spent in rent over the last 5 years? It adds up… and where does that money go? Into someone else’s home equity.

If you’re considering whether to rent or buy in Toronto why not do the math yourself. Consider the above chart like your own rent vs buy Toronto calculator and crunch the numbers yourself.

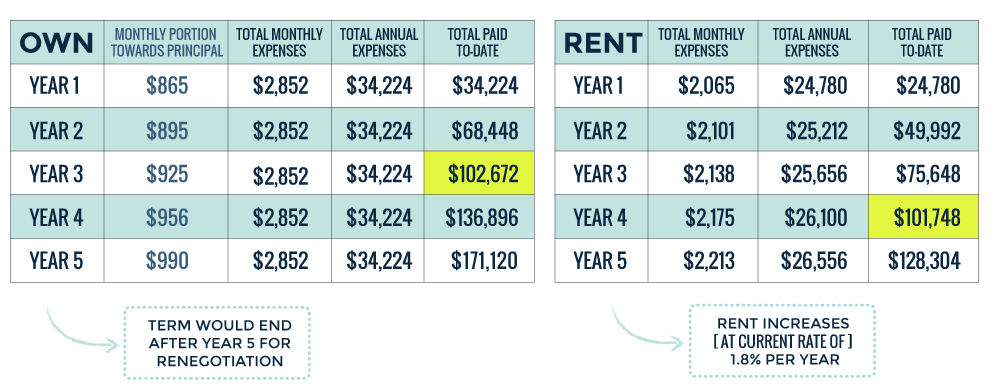

Now, let’s compare your living expenses on the upcoming years on this same property.

After just 3 years of owning, you’ll have paid $102,672 towards your property and living expenses. After just 4 years of renting, you’ll have paid about the same, totalling out at $101,748 in living expenses. The only difference is that this money hasn’t built you any equity. It’s paying someone else’s mortgage.

Let’s assume the market goes up 5% each year (though that’s a modest growth rate given the market’s performance these past few years). The value of your property after 4 years will have gone from $500K to $600K. This means that you’ve not only gained over $100K in equity but you’ve also paid off your mortgage to the tune of $43,692. So that 4 years has earned you $143,692 total equity.

Over the past year the downtown Toronto real estate market has seen impressive gains and tightened market conditions. This has had quite the effect on Toronto’s rental market and its extremely low vacancy rates. The cost of renting in Toronto just keeps climbing and as it does it makes the rent vs buy debate that much more important for would-be first-time buyers looking to break into the Toronto market.

*Our fresh take on the Rent vs Buy in Toronto debate with an eye towards the future.

Buying a home versus renting, which is right for you? Use this rent or buy calculator to make the calculation easy and refer to the charts above for context.

The point of this article is to illustrate where the money goes when you compare the cost of renting versus buying in Toronto. So if you’re planning on living in the same place for more than seven years, it may make more sense financially to own vs rent. Ultimately, it depends on your lifestyle, your goals, and whether or not you have the means to buy.

If the flexibility and freedom of renting suits your needs right now, there’s no harm in that. Choosing to buy is a long term plan, but it’s also a great way to save for your future. So while you may not be ready to buy, I do encourage you to start saving. Toronto’s condo market is thriving and the longer you wait, the less your money is worth. You can read more on why The Best Day to Buy Real Estate is Yesterday on our blog.